How to Choose the Right Business Banking Partner in the UAE

Choosing the right business banking partner is a foundational step for any SME in the UAE. It’s the operational hub for everything from client payments to payroll. But what happens when even a strong banking relationship isn't enough to fuel your growth ambitions?

Even with the best business banking, cash flow gaps still exist. This is where solutions like Comfi help SMEs get paid faster.

Why a Great Bank Account Is Only Half the Story

Many successful businesses in the UAE encounter a common paradox: sales are climbing and the order book is full, yet cash flow remains uncomfortably tight. This isn't a reflection of your bank's performance; it's a natural consequence of B2B commerce and its long payment cycles.

At its core, a bank’s job is to store money safely. It acts as a secure vault, protecting your capital and ensuring your transactions are processed smoothly. What a traditional bank isn't designed for is accelerating your access to the money you've already earned but that remains locked in outstanding invoices.

This distinction is critical for any ambitious SME.

- A bank stores money: It provides the essential infrastructure for deposits, payments, and financial stability.

- A solution like Comfi unlocks money: It works in partnership with your bank to convert your unpaid invoices into usable cash, right now.

This is where the narrative of business growth often hits a snag. Even with the best business banking services, a company waiting 30, 60, or even 90 days for payment can miss out on crucial opportunities—like purchasing new inventory, funding a key project, or hiring essential staff. Managing your bank account is just one piece of the financial puzzle. You must also manage your receivables, which means finding ways to shorten that waiting period. To explore tools that can assist, check out our guide on accounting software in the UAE.

The fundamental challenge isn't about having money; it's about accessing it when you need it most. Your bank stores your money, but a solution like Comfi gives you the key to unlock that capital and get paid faster.

What To Expect From Core Business Banking Services

When evaluating a business banking partner, it’s easy to get lost in marketing materials. A more practical approach is to focus on the core services that will directly impact your day-to-day operations and cash management.

The business current account is the cornerstone of your financial operations. Look beyond the brand name and dig into the details. What are the transaction limits? How effectively does it integrate with your accounting software? For an e-commerce business, this seamless connection can save hours of manual data entry each week. A key part of managing this is knowing how to reconcile bank statements accurately to maintain clear financial records.

For many SMEs, merchant services are another non-negotiable feature. If you accept card payments, you need to compare not only the processing fees but also the settlement times. How quickly does the money from a customer's purchase actually land in your account? A delay of even a few days can create significant liquidity challenges.

Evaluating Services For Your Business Model

The ideal combination of banking services is entirely dependent on your business model. There is no one-size-fits-all solution.

An electronics distributor importing goods will prioritise trade finance facilities to manage documentation and customs payments. In contrast, a B2B software company will be more focused on finding reliable, low-fee merchant processing for online subscriptions.

Your bank provides the vault to store your money securely. However, when B2B payment delays create cash flow gaps, you need a key—not another vault. Even the best bank account cannot shorten a 90-day payment term.

This gets to the heart of the matter for businesses in the UAE. A solid business bank is essential for holding and managing capital. But when that capital is trapped in unpaid invoices, a different kind of solution is needed to get it moving again.

Must-Have Features of a Modern Banking Partner

In today's digital economy, the difference between a bank that simply holds your money and one that actively supports your growth is clear. A simple place to park cash is no longer sufficient. You need a banking partner that functions as a central hub for your entire operation, providing a competitive advantage.

A seamless digital banking platform is non-negotiable. This means more than just a mobile app for checking your balance. A powerful platform should offer intuitive cash flow forecasting tools, easy multi-user management with customisable permissions, and robust security that protects your assets without creating unnecessary friction.

Going Beyond Basic Digital Access

A slick user interface is only the beginning. For any modern SME, API accessibility is a game-changer. An open API allows your bank account to communicate directly with other critical business tools.

- Accounting Integration: Connect directly to software like Xero or QuickBooks to automate bank reconciliation, saving dozens of hours of manual data entry each month.

- Payment Gateways: Smooth integration with payment processors ensures faster, error-free settlements, eliminating the need to chase down mismatched transactions.

- Custom Solutions: APIs enable you to build internal dashboards that pull real-time banking data, empowering you to make smarter, faster decisions.

Understanding the tools that power modern finance is a significant advantage. Learning about fintech software development can provide insight into how these digital features are built and why they are so vital for your operations.

Finally, never underestimate the value of a dedicated relationship manager who understands your industry. A manager familiar with the seasonal cash flow patterns of a retail business or the subscription model of a SaaS company can offer relevant advice that a generic call centre cannot.

This combination of knowledgeable people and powerful digital tools distinguishes a true growth partner from a simple bank.

How to Navigate Banking Fees and Paperwork

Hidden costs and administrative burdens can quickly undermine an otherwise positive business banking relationship. In the UAE, gaining a clear understanding of fee structures and paperwork requirements upfront is essential for protecting your bottom line.

Many business accounts include charges for everyday activities, such as international transfers, falling below a minimum balance, or even basic account management. A practical first step is to analyse your company’s typical monthly transactions. If you frequently make international payments, seek an account with competitive foreign exchange rates and low transfer fees. These small percentages can add up to a significant sum over a year.

Understanding the Essential Documents

Preparation is key when opening an account. While specific requirements may vary between banks, having the core documents ready will expedite the process.

For most SMEs setting up in the UAE, you will need the following:

- A valid Trade License for your business.

- Your company's Memorandum of Association (MOA).

- Passport copies and residency visas for all shareholders.

- The Emirates ID of all account signatories.

It’s worth noting that the local banking sector is incredibly robust. UAE banks demonstrated impressive profitability, which creates a stable environment where traditional banks can work effectively alongside fintech innovators. You can discover more about the GCC banking landscape from EY's report.

Being organised with your paperwork does more than just open an account; it establishes a foundation of credibility with your banking partner. A smooth onboarding process sets a positive tone for the entire relationship.

Getting these details right is a fundamental part of establishing your business's financial footing. It’s as important as understanding your eligibility for other financial products, as it ensures you start on solid ground.

Bridging the Gap When Your Bank Is Not Enough

You have done everything right. You've selected a solid banking partner, sales are growing, and your business is on an upward trajectory. So why does it still feel like you’re constantly chasing cash?

This is a common challenge for countless SMEs, and it doesn't mean your business banking setup has failed.

The reality is, even the best bank account cannot shorten a 90-day payment term from a major client. Your bank is designed to be a secure vault for your money after it arrives. It cannot, however, provide a key to unlock the capital that’s tied up in your accounts receivable. This is where a critical cash flow gap emerges, preventing you from seizing new opportunities as they arise.

From Stored Capital to Unlocked Capital

Imagine a wholesaler in Dubai who lands a massive order from a well-known retailer. It’s a game-changing deal, but there’s a problem. Most of their working capital is locked in unpaid invoices from previous orders, leaving them unable to afford the inventory needed to fulfil this new opportunity.

This is precisely where innovative solutions work alongside your bank to bridge that gap. The distinction is simple yet powerful:

- Your Bank Stores Money: It holds your funds securely, processes payments, and provides stability.

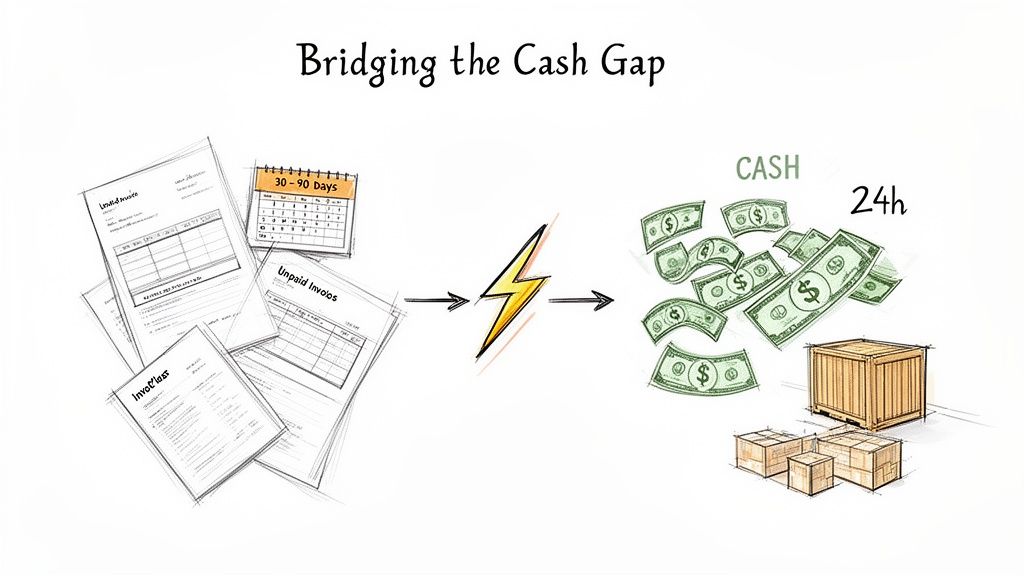

- A Solution Like Comfi Unlocks Money: Our clients have been able to get immediate access to the cash from their invoices, turning a 30-90 day wait into cash-in-hand within 24 hours.

The core problem for many growing SMEs isn't a lack of sales; it's a lack of liquidity. Unlocking your working capital means you can say "yes" to bigger orders, invest in growth, and operate with confidence.

The financial sector in the UAE is highly liquid. This robust environment creates the perfect conditions for fintech solutions to complement traditional banking.

By getting paid faster on invoices, you transform your receivables from a figure on a balance sheet into real, usable capital. This approach doesn't replace your bank; it enhances its value by ensuring your vault is never empty due to slow-paying customers. Exploring how this synergy works can be a game-changer; you can learn more about the evolution of fintech in our detailed guide.

Your Top UAE Business Banking Questions, Answered

Navigating the world of business banking in the UAE can feel complex. There are many terms, requirements, and options to understand. To provide clarity, let's address some of the most common questions from business owners.

What Are the Minimum Balance Requirements for SME Accounts?

This varies significantly. Newer, digital-first banks often promote zero-balance accounts, which can be a great option for startups.

Conversely, many established banks may require an average balance of AED 50,000 or more. It is crucial to understand that falling below this minimum will result in a penalty fee. Be sure to ask about this upfront—incurring unnecessary monthly fees because a bank's rules don't align with your cash flow is a frustrating and avoidable expense.

How Is Invoice Discounting Different From a Business Loan?

This is an important distinction that can fundamentally change how you manage your finances. A business loan is debt. You borrow money, which appears as a liability on your balance sheet, and you must repay it with interest.

Invoice discounting is not a loan. It is the sale of your unpaid customer invoices to a third party for a fee. This process unlocks the cash you are already owed, often within a day or two.

Think of it as fast-forwarding your revenue. You gain immediate access to your own working capital without taking on debt, making it an incredibly flexible tool for closing cash flow gaps.

Can I Switch Business Banks If I Am Unhappy?

Yes, you can. You are never locked into a single provider. However, the transition must be managed carefully to avoid operational disruptions.

The recommended approach is to open your new bank account before closing the old one. Once the new account is active, you must update all your clients and suppliers with the new details. Don't forget to transfer any direct debits or recurring payments. While it requires some administrative effort, moving to a bank that better understands and supports your business needs is well worth it in the long run.

Even with a great business banking partner, waiting on customer payments can slow your growth. Comfi helps SMEs unlock the cash tied up in unpaid invoices—often in just 24 hours. See how we can help you grow without limits at https://comfi.ai.