A Guide to Terms of Payment for MENA Businesses

A term of payment is the agreement you make with a customer about when and how they will pay your invoice. It’s much more than just a due date; it’s a core component of any business transaction that directly shapes your cash flow, your risk exposure, and the very nature of your relationship with your buyers.

What is a Term of Payment in Business

Think of payment terms as the financial rulebook for a sale. These are the agreed-upon conditions that dictate how a buyer pays a seller for products or services. While it sounds simple, this agreement is one of the most powerful tools for managing your company's financial health.

For small and medium-sized businesses (SMEs) across the MENA region, mastering these terms is absolutely critical. Clear, well-defined payment terms eliminate confusion, reduce the risk of late payments, and establish a professional tone from the outset. They are the foundation of a solid buyer-seller relationship.

Why Payment Terms Are Crucial for Your Business

The impact of your payment terms extends far beyond just getting paid on time. Setting them is a strategic decision that affects your company's liquidity, competitiveness, and daily stability. When you offer credit to your clients, you are essentially letting them use your funds for a short period.

That decision has tangible consequences. Flexible terms might attract more customers, but they can also put a serious strain on your cash flow. You could find that clients were able to unlock their working capital at the expense of your own, leaving you short on funds for inventory, payroll, or new growth opportunities. Conversely, being too strict can deter potential buyers who need or expect more flexible arrangements.

A well-structured term of payment strikes the right balance between securing your cash flow and meeting the commercial realities of your industry. It protects your business while building trust and goodwill with your clients.

Ultimately, mastering your payment terms is about taking control of your financial future. It’s how you create a predictable stream of income that keeps your business running smoothly and allows you to plan ahead with confidence.

Key Components of Payment Terms

To be effective, your payment terms must be crystal clear, leaving no room for ambiguity. While the wording can vary, several core details should always be present.

Make sure your payment terms always spell out:

- The Due Date: The exact timeframe for payment. This could be "Net 30" (due in 30 days) or "Due upon receipt."

- Payment Method: How you accept payment. Be specific: bank transfer, cheque, or specific online payment gateways.

- Early Payment Discounts: Any incentives you offer for paying ahead of schedule. A classic example is "2/10 Net 30," which gives a 2% discount if the bill is paid within 10 days.

- Late Payment Penalties: The consequences for missing the due date. This might include interest charges or a flat late fee.

By outlining these elements on every invoice and contract, you build a transparent framework that protects both you and your customer. It’s a simple step that ensures a much smoother transaction from start to finish.

Decoding Common Payment Terms for Your Business

To truly get a grip on your business finances, you must first speak the language. Payment terms are a huge part of that language. Think of them as the ground rules for how and when money moves between you and your customers. Getting these right directly impacts how much cash you have on hand to run your business day-to-day.

For any SME trying to grow in the MENA region, knowing these terms inside and out isn't just helpful—it's essential for survival and long-term success.

Let's walk through the most common payment terms you'll encounter. We'll skip the dry, textbook definitions and focus on what they actually mean for your business in the real world. That way, you can determine what makes the most sense for you.

Getting a Handle on Net Payment Terms

Net terms are the foundation of most B2B transactions. The number following "Net" is simply the number of days your customer has to pay their invoice in full. So, Net 30 means the clock starts ticking on the invoice date, and the full amount is due within 30 days. It’s arguably the most common term because it strikes a decent balance—the buyer gets some breathing room, and the seller gets paid relatively quickly.

But you'll see a few variations, and each one changes the dynamic for your cash flow.

- Net 7, 15, or 30: These shorter windows are great for smaller sales or when you're dealing with a new client and still building trust. They help you convert sales into cash much faster.

- Net 60 or 90: You usually reserve these longer terms for your large, trusted clients or for industries with long project timelines. Offering Net 60 might help you land a larger contract, but be prepared for the trade-off. You're agreeing to wait two or three months for your money, which can put a serious strain on your own finances.

Choosing the right Net term is a balancing act. You have to weigh the appeal of making a sale against your own ability to maintain operations while you wait to get paid. You can dig deeper into this by exploring the pros and cons of credit terms vs prepayment discounts, which often push customers to pay faster.

The term of payment you set is a direct reflection of your company's financial strategy. It communicates your expectations, manages your risk, and ultimately determines how quickly your sales turn into usable cash.

Exploring Other Common Terms

Beyond the standard Net terms, a few other arrangements appear frequently, especially across the diverse markets in the MENA region. Each one is designed for a different situation, catering to specific business models, risk levels, and customer relationships.

Knowing these alternatives gives you more flexibility and makes your sales strategy much smarter.

Cash on Delivery (COD)

This one is exactly what it sounds like. With Cash on Delivery (COD), the customer pays for the goods the moment they arrive. For you, the seller, this is as low-risk as it gets. There's no waiting period and virtually no chance of a customer defaulting on a payment. It's a go-to option for e-commerce and for one-off sales to new customers without an established payment history. The only downside is that it can be a hassle for the buyer, who needs to have the cash ready.

End of Month (EOM)

End of Month (EOM) terms add a twist to the Net formula. If you see "Net 30 EOM," it means the payment is due 30 days after the end of the month the invoice was sent. For example, an invoice dated March 5th would be due on April 30th (30 days after the end of March). This is a favorite for buyers who prefer to process all their payments in one batch at the end of the month, but for you, it can mean waiting even longer for your cash.

The Rise of Buy Now, Pay Later (BNPL)

One of the biggest shifts in payments is the explosion of Buy Now, Pay Later (BNPL). It began as a consumer trend but is quickly making its way into the B2B world. BNPL allows buyers to receive their products immediately but splits the cost into several smaller, often interest-free, payments.

This model has taken the Middle East by storm. BNPL services have completely changed how people pay, especially in the UAE, Saudi Arabia, and Bahrain. They offer a simple way to break up purchases into manageable installments without needing a credit card. In fact, Mastercard found that 85% of MENA residents tried an emerging payment method like BNPL in the last year alone. This has fueled a massive boom, with regional players like Tamara and Tabby now serving millions of customers.

For a business, offering a BNPL option can be a game-changer. It removes the sticker shock for buyers, making it easier for them to commit to larger purchases and boosting your sales in the process.

How Payment Terms Impact Your Cash Flow

The term of payment you choose is much more than a small detail on an invoice. It's one of the most powerful levers you can pull to manage your business's financial health. Every choice, whether demanding payment upfront or offering generous credit, creates a ripple effect on your day-to-day operations.

For example, offering lenient terms like Net 60 might seem like a smart move to land a big client. But in reality, it opens up a huge gap between when you deliver your product or service and when the cash actually hits your bank account. On the other hand, sticking to strict terms like Payment in Advance (PIA) protects your cash flow but might make you less competitive, possibly pushing potential customers away.

This is the tightrope every SME in the region must walk: finding that sweet spot between driving sales and keeping the lights on.

The Cash Flow Balancing Act

When you extend payment terms, your revenue remains a number sitting in your accounts receivable. You’ve already delivered the goods or services, paid your own suppliers, and covered payroll, but your cash is tied up until that invoice gets paid.

This delay creates a cash flow gap—the time between spending money and getting paid for it. The longer your payment terms, the wider that gap gets, which can seriously strain your ability to manage daily expenses or jump on new opportunities.

The real risk of a generous term of payment isn't just the wait; it's the uncertainty. A delayed payment can throw your financial forecasts into chaos, and a default can turn a profitable deal into a painful loss.

Getting a handle on this means truly understanding accounts payable and accounts receivable, because these two ledgers are the heartbeat of your cash flow cycle.

Assessing Client Reliability and Risk

Before you even think about offering credit, you need to get a sense of your client’s financial reliability. It’s one thing to offer terms to a long-term partner with a perfect payment record; it’s another entirely to give them to a brand-new customer you know nothing about. A simple, consistent policy is your best friend here.

Here are a few practical steps to start managing credit risk:

- Credit Application: Have new clients fill out a standard credit application form. This should gather basic business details, trade references, and their consent for a credit check.

- Trade References: Actually call the references they provide. Ask them directly about the client’s payment habits. Are they on time? Do they consistently pay late?

- Tiered Term Structure: Don't offer your best terms right out of the gate. Create a policy where payment terms improve as the relationship grows. A new client might start with PIA or Net 15, and only graduate to Net 30 after a few successful, on-time payments.

This structured approach lets you build trust and reward good clients without putting your own business on the line.

Creating a Policy That Protects You

Your payment term policy shouldn’t be an unspoken rule; it needs to be a clear, written document. This gives your sales and finance teams a playbook to work from and removes the guesswork when negotiating with customers. Think of it as your first line of defense against late payments.

A solid policy should clearly outline:

- Standard Terms: What are your default payment terms? For most, this is Net 30.

- Conditions for Extended Terms: What does a client need to do to earn longer terms like Net 60? This could be based on order size, their history with you, or creditworthiness.

- Late Payment Procedures: What happens when an invoice is overdue? Define the steps, from a friendly reminder email to late fees and final warnings.

By setting these rules down on paper, you create a framework that empowers your sales team to close deals without gambling with your financial stability. Many businesses are also exploring modern payment solutions to offer flexibility without taking on all the risk themselves. For instance, exploring how B2B Buy Now, Pay Later enhances cash flow can open up new ways to stay competitive and financially healthy.

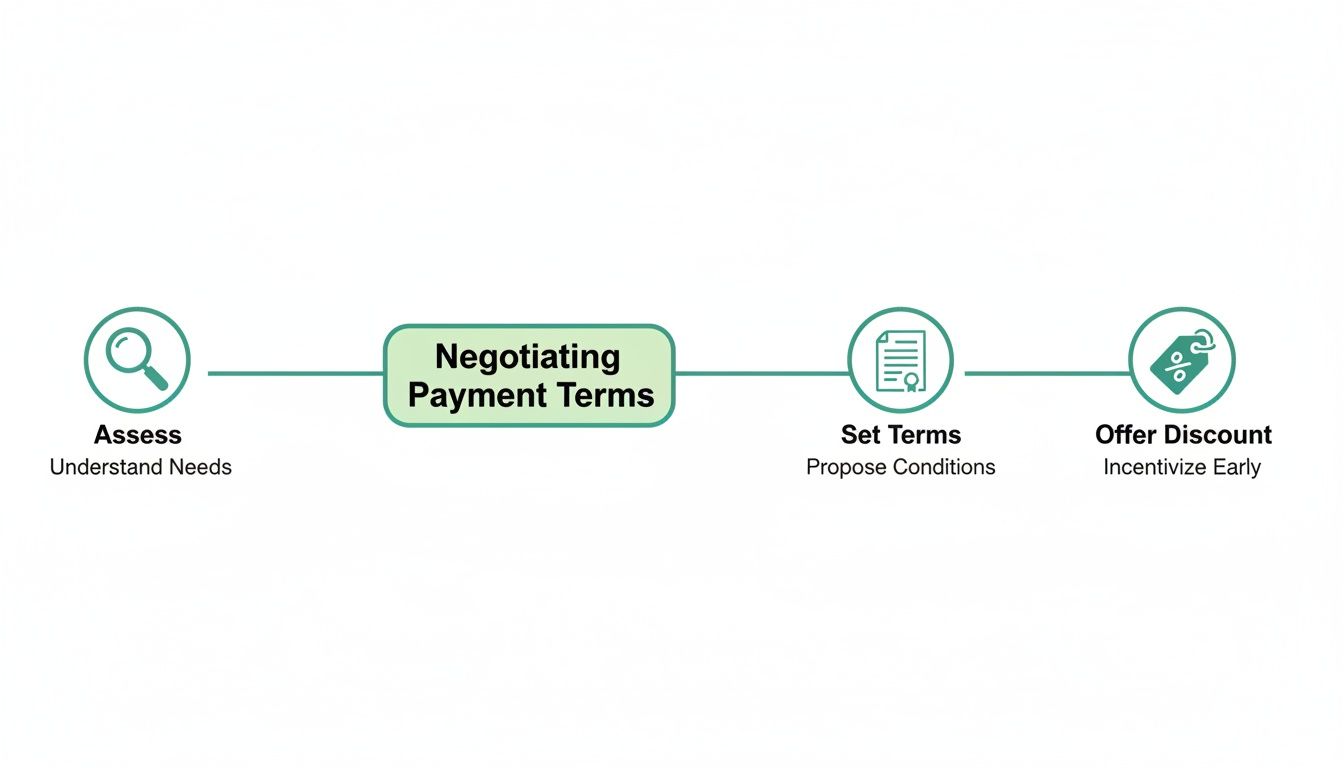

How to Set and Negotiate Better Payment Terms

Setting your term of payment isn't just another box to check on your paperwork. It’s a strategic move that directly protects your cash flow and builds a stronger business. Think of your payment policy as the financial rulebook for every deal you make—it sets expectations upfront and keeps misunderstandings from turning into major headaches.

The trick is finding that sweet spot: terms that are firm enough to keep your finances healthy but flexible enough to attract and keep great customers. Nailing this balance is fundamental to growing your business sustainably.

Creating Your Payment Policy

Before you even think about negotiating, you need a solid starting point. Your standard payment policy shouldn't be a random guess. Simply choosing "Net 30" because it sounds standard is a recipe for trouble. Instead, a strong policy comes from a careful analysis of your own business and the market you operate in.

Here’s what you need to seriously consider:

- Industry Norms: What's typical in your field? Knowing the standard provides a benchmark. While it helps to be competitive, don't feel locked in—if your cash flow can't handle long payment cycles, you need to set stricter terms.

- Your Financial Position: This is the most important factor. How long can you realistically wait to get paid? You need to dig into your own cash flow cycle and determine the absolute longest you can extend credit without putting your own operations at risk.

- Customer Relationships: Trust and history matter. A loyal, long-term client who always pays on time has earned more flexibility. A brand-new customer, on the other hand, should start with stricter terms until they've proven their reliability.

Thinking through these factors helps you build a baseline policy that’s both reasonable for your customers and financially sound for you. This becomes your anchor, giving you a confident position to negotiate from.

Powerful Negotiation Tactics

Remember, negotiation is a conversation, not a battle. You're looking for a win-win solution. One of the simplest and most effective tools you have is the early payment discount. This small incentive can work wonders for your cash flow by giving customers a compelling reason to pay you sooner.

The classic "2/10 Net 30" term is a fantastic example. It tells the customer they can take a 2% discount if they pay within 10 days; otherwise, the full amount is due in 30 days. For them, it’s a simple way to save money. For you, it's a powerful way to get cash in hand weeks ahead of schedule.

But what happens when a big, important client demands longer terms like Net 60 or even Net 90? This is a situation almost every SME faces. It’s tempting to cave just to land the contract, but you have to know your limits. If waiting that long for payment will squeeze your business, you need to be ready to stand firm or suggest a different approach.

Communicating Your Terms Clearly

Once you’ve settled on your terms, crystal-clear communication is non-negotiable. Confusion is the number one cause of late payments. Your terms need to be spelled out explicitly on every single invoice, contract, and sales agreement.

Make sure your documents clearly state:

- The total amount due.

- The precise due date (e.g., "Due by October 15, 2024").

- Any details about early payment discounts.

- The consequences for paying late, like specific fees or interest.

This level of transparency sets a professional tone right from the start. It ensures everyone is on the same page, turning the payment process from a potential point of conflict into a smooth and predictable part of doing business.

Time to Rethink B2B Payments: Moving Beyond Old-School Terms

The way businesses pay each other is finally catching up with the rest of the world. Gone are the days of paper invoices and waiting weeks for a check to clear. This shift is especially powerful in the B2B space across the Middle East and Africa (MENA), where new technology is compressing payment cycles that once took months into something that happens in minutes.

This isn't just about convenience; it's a fundamental change in business strategy. Modern payment solutions give suppliers the power to offer flexible terms to their buyers without strangling their own cash flow. It’s all about finding a smarter approach to the term of payment—one that works for everyone involved.

The B2B payments market in the MENA region is exploding, currently valued at over USD 70 billion and on track to more than double. This incredible growth is fueled by real-time payment technologies that turn the traditional 30-90 day wait for wires and checks into nearly instant transfers. As key industries like manufacturing, IT, F&B, and retail grow, so does the pressure for faster, more efficient cash management.

Moving Past Traditional Credit Terms

For decades, the standard playbook for a B2B term of payment was simple: suppliers acted as the financiers. They extended payment terms directly to their buyers, offering Net 30, 60, or even 90-day terms and then simply waited. While this gesture might help land a bigger deal, it places all the financial pressure squarely on the supplier's shoulders. They’re left to manage credit risk, chase late payments, and deal with the operational headache that comes with it.

But what if there was a better way? Modern solutions are flipping this outdated model on its head. Instead of suppliers tying up their own cash, specialized platforms can step in to bridge that financial gap. This simple change allows suppliers to get their cash right away while buyers still get the payment flexibility they need to run their own businesses.

The core principles of setting smart payment terms—assessing risk, being clear, and maybe offering an incentive—are still essential. The graphic below breaks down these timeless steps, which are just as important when you layer in modern payment tools.

The Rise of B2B Buy Now, Pay Later

One of the most significant changes we're seeing is the adoption of B2B Buy Now, Pay Later (BNPL). It’s a concept most of us know from online shopping, but it’s been adapted for business-to-business transactions with incredible results. The genius of B2B BNPL is that it separates two distinct events: the supplier getting paid and the buyer making their payment.

Here’s a quick look at how it works:

- A supplier sells goods to a buyer and sends an invoice, just like always.

- But instead of waiting, the supplier uses a platform that pays them the full invoice amount, often within a day.

- The buyer then has the freedom to pay the platform back later, based on the terms they agreed on (like in 30 or 60 days).

This approach effectively decouples the supplier's need for immediate cash from the buyer's need for flexible payment terms. Both parties get what they need to operate efficiently.

Platforms like Comfi are built to handle exactly these kinds of arrangements. They empower suppliers to get paid upfront while letting their buyers pay on a timeline that works for them. By using such platforms, both businesses have found they were able to unlock precious working capital and operate more efficiently. The supplier is shielded from late payment risk, and the buyer gets the breathing room they need to manage their own inventory and cash flow. To get the most out of this, exploring the benefits of automated invoice processing can slash manual work and reduce errors even further.

A True Win-Win for Suppliers and Buyers

This modern take on the term of payment creates a scenario where everyone genuinely wins. It breaks free from the limitations of traditional credit and helps build a more dynamic, resilient, and collaborative supply chain.

For suppliers, the advantages are immediate and impactful:

- Instant Cash Flow: Get paid in as little as 24 hours. No more waiting, no more uncertainty.

- Zero Credit Risk: The burden of a customer paying late—or not at all—is completely removed.

- More Sales: Offering flexible terms can be a huge competitive advantage, attracting new customers and encouraging larger orders.

Buyers see major benefits, too:

- Protected Working Capital: They can buy the inventory or materials they need, right when they need them, without draining their bank accounts.

- Stronger Supplier Relationships: They can meet their business needs without putting their suppliers in a tough financial spot.

- Simple Purchasing: The process is typically seamless and integrates directly into how they already buy.

To give you a clearer picture, let's compare the old way with the new way.

Comparing Traditional vs Modern B2B Payment Solutions

This comparison highlights the key differences in cash flow impact, risk, and efficiency between traditional payment terms and modern solutions like those facilitated by Comfi

- Cash Flow for Supplier

- Traditional Net 30/60 Terms: Delayed; cash is tied up for 30-90 days.

- Modern Solutions (e.g., Comfi): Immediate; cash received within 24-48 hours.

- Credit Risk for Supplier

- Traditional Net 30/60 Terms: High; supplier bears all the risk of non-payment.

- Modern Solutions (e.g., Comfi): Zero; the platform assumes the risk.

- Cash Flow for Buyer

- Traditional Net 30/60 Terms: Positive; allows buyer to sell goods before paying.

- Modern Solutions (e.g., Comfi): Positive; buyer gets the same (or better) payment flexibility.

- Sales Impact

- Traditional Net 30/60 Terms: Can limit sales if terms aren't competitive.

- Modern Solutions (e.g., Comfi): Can boost sales by offering attractive, flexible terms.

- Operational Effort

- Traditional Net 30/60 Terms: High; requires credit checks, collections, and follow-ups.

- Modern Solutions (e.g., Comfi): Minimal; the process is automated and handled by the platform.

- Relationship Dynamic

- Traditional Net 30/60 Terms: Can become strained due to payment chasing.

- Modern Solutions (e.g., Comfi): Strengthened; focuses on the business, not the payment.

As you can see, the shift isn't just about speed; it's about creating a healthier financial ecosystem for everyone.

By adopting these modern solutions, businesses aren't just processing payments faster—they're building stronger, more sustainable commercial relationships.

To dig deeper, check out our guide on https://comfi.ai/blog/digital-b2b-payments, which offers more detail on how these technologies are reshaping B2B commerce.

Common Questions About Payment Terms Answered

When you're juggling all the moving parts of a business, payment terms can feel like just one more thing on your plate. But getting them right is crucial. Here are some straightforward answers to the questions we hear most often from business owners.

What’s the Smartest Payment Term for a Brand New Business?

When you’re just starting out, cash is king. It’s tempting to offer generous payment terms to land those first crucial customers, but that can be a risky move. Your number one priority has to be protecting your cash flow.

Here are a few solid options to start with:

- Payment in Advance (PIA): This is your safest bet. It completely removes the risk of not getting paid, which is perfect for custom jobs or big first-time orders where you have significant upfront costs.

- Cash on Delivery (COD): If you're selling physical products, COD is a fantastic way to go. You get paid the second the customer gets their hands on the goods. Simple, clean, and no waiting.

- Net 7 or Net 15: If you feel you need to offer some credit to be competitive, keep it tight. A short window like 7 or 15 days lets you build a payment history with a new client without tying up your precious working capital for too long.

My advice? Start strict. A new business should always begin with the tightest terms possible. Once a customer proves they are reliable and pays on time, you can always choose to offer them more flexibility as a reward.

How Do I Handle Late Payments Without Losing a Customer?

Chasing late payments is never fun, but it's a necessary part of business. The trick is to handle it with a process that's firm, professional, and consistent—not emotional.

A step-by-step approach works best:

- The Gentle Nudge: Set up an automated email to go out the day the invoice is due. You’d be surprised how often a friendly reminder is all it takes.

- The Personal Touch: A few days past due? It’s time for a personal email or a quick phone call. This signals you're on top of it while keeping the conversation friendly and open.

- The Formal Notice: If the invoice is now seriously late (say, 15 days), your next communication should be more formal. This is where you mention the late fees you hopefully outlined in your original term of payment.

- The Final Demand: If you're still met with silence, a final demand letter clearly states what next steps you'll be forced to take.

The goal is always to get paid, but the secondary goal is to keep the relationship intact if you can. A clear process helps you do both.

Can I Change the Payment Terms for a Client I Already Work With?

Absolutely. In fact, you should. Business relationships aren't static, and your payment terms shouldn't be either.

Think of it this way: if you have a fantastic, long-term client who has never missed a payment, why not reward them? Bumping them from Net 30 to a Net 45 can strengthen that relationship and might even encourage them to place larger orders.

On the flip side, if a once-reliable client suddenly starts paying late, you have every right to protect your business by shortening their terms. The golden rule here is communication. Never just spring the change on them. Have a conversation, explain your reasoning, and get the new terms in writing. A little transparency goes a long way in preventing future headaches.

Ready to offer flexible payment terms without risking your cash flow? Comfi helps you get paid upfront while your customers pay later. Discover how our platform can help your business at https://comfi.ai.

Related Reading

- B2B Payments

- Solve Creative Agency Late Payment UAE Issues

- How Payment Default Dents Small Business Growth and Survival

- A Guide to B2B Payment Solutions for MENA Businesses

Looking to improve your cash flow? Explore Comfi's Buy Now Pay Later solutions. Get started today.