7 Ways to Access Instant Business Funding in 2026

For small and medium-sized enterprises (SMEs) in the UAE, managing cash flow is a constant balancing act. Waiting 30, 60, or even 90 days for invoice payments can stall growth, delay inventory purchases, and limit your ability to seize new opportunities. But what if you could access the value of your invoices or secure capital almost immediately? This is the promise of instant funding.

In this guide, we'll explore what 'instant' really means in the world of business capital, moving beyond traditional, slow processes. We will break down seven modern, accessible ways for your business to secure the funds it needs to thrive in 2026. Each option is presented with clear explanations, direct links, and screenshots to simplify your decision-making. We will compare digital platforms that are reshaping how MENA businesses manage their finances and accelerate their growth, helping you find the right solution so that clients were able to unlock their working capital and get ahead.

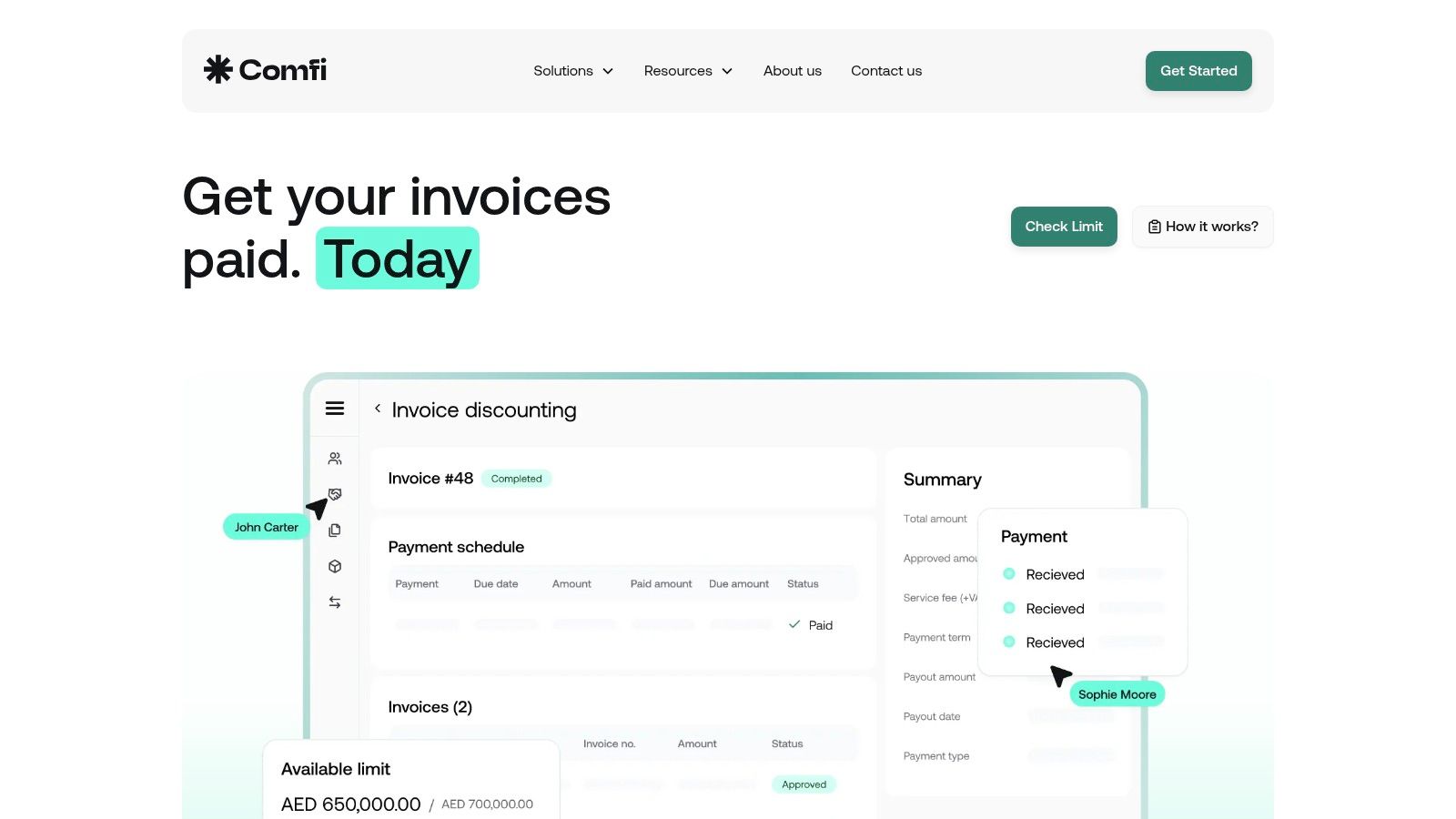

1. Comfi

Comfi has established itself as a leading choice for businesses in the MENA region seeking reliable and instant funding solutions. Its platform is specifically engineered for B2B transactions, providing a powerful suite of tools like invoice discounting and extended payment terms (Buy Now, Pay Later) for wholesalers, distributors, and marketplaces. The core value lies in its ability to accelerate cash flow for suppliers by providing upfront payments for their invoices, while offering buyers flexible 30, 60, or 90-day payment options.

This model effectively decouples the supplier's need for immediate cash from the buyer's need for payment flexibility. By managing the collections process, Comfi allows businesses to focus on growth activities like securing larger deals and acquiring new customers, rather than chasing outstanding payments. The platform's digital-first approach ensures a seamless user experience from start to finish.

Key Strengths and Use Cases

Comfi stands out due to its impressive approval rate and measurable impact on business performance. With an 85% approval rate, it provides accessible support for a wide range of SMEs. Clients report tangible benefits, such as a 30% increase in average order size and a 20% uplift in new customer acquisition, demonstrating the platform's direct contribution to revenue growth. The fully digital onboarding, including an instant eligibility check, means approved invoices are typically paid within 24 hours.

Practical Applications:

- Inventory Management: A distributor can use Comfi to receive funds for its invoices immediately, allowing them to stock up on high-demand inventory without waiting for customer payments to clear.

- Winning Larger Deals: A B2B supplier can confidently offer 60-day payment terms to a major new client, knowing Comfi will provide the funds upfront, securing a deal that might otherwise be lost due to cash flow constraints.

- Marketplace Integration: An e-commerce marketplace can embed Comfi's payment options directly into its checkout process using low-code plugins or APIs, offering instant terms to all its buyers and increasing sales velocity for its vendors.

Platform and Pricing Details

- Pros: Very fast access to cash (paid within 24 hours); High, SME-friendly approval rate (~85%); Removes collections burden from suppliers; Seamless integration via dashboard, plugins, and API.

- Cons: Pricing is not publicly listed and is tailored after an eligibility check; Primarily focused on MENA-based SMEs.

For more information or to check your eligibility, visit the official website.

Website: https://comfi.ai

2. Beehive

Beehive is a leading peer-to-peer platform in the UAE, designed to connect established SMEs with investors for working capital and invoice finance needs. While not offering literal "instant funding" within minutes, it provides a significantly faster alternative to traditional banks, with decisions and funding typically processed within a few days. Its 100% online application process is streamlined to minimise paperwork, making it a practical choice for businesses needing efficient access to capital.

What makes Beehive unique is its strong regional focus and recognition. As a pioneer in the region's SME finance space, it is regulated by the DFSA (Dubai Financial Services Authority) and recognised by Dubai SME. This provides a layer of trust and credibility. Their marketplace model also means funding comes directly from a community of investors, which can sometimes lead to more flexible and competitive terms than a single institutional source might offer.

Key Features and Insights

- Product Offerings: Beehive specialises in two core products - Invoice Finance, allowing you to get paid on your outstanding invoices early, and Term/Working Capital products for broader business needs.

- Application Process: To use the platform, SMEs submit an online application. Beehive’s credit team then assesses the business's risk profile before listing the funding request on the marketplace for investors.

- Pricing: Costs are transparent but variable. The rates and fees depend on your business's risk assessment, so you must complete an application to receive a specific offer.

- Pros: Faster than banks; strong reputation in the UAE and GCC.

- Cons: Funding takes days, not hours; pricing is not disclosed upfront.

Practical Insight: To get the fastest results on Beehive, ensure all your financial documents are organised and ready for upload before you start the application. This preparation can significantly speed up the verification and approval process.

Find out more at Beehive.

3. Funding Souq

Funding Souq is a prominent debt-funding platform offering Sharia-compliant SME business arrangements across the UAE and Saudi Arabia. While it doesn't provide literal "instant funding" in minutes, it presents a much faster route to capital than traditional banking, with approvals often occurring within 72 hours. Its fully digital application process is designed to be quick and straightforward, making it an excellent option for businesses needing efficient access to funds.

What makes Funding Souq unique is its strong regulatory foundation and specialised Sharia-compliant offerings. The platform is regulated by the DFSA in the DIFC and holds a SAMA licence in Saudi Arabia, providing a high level of credibility. This dual-region presence makes it a go-to for GCC-based businesses looking for growth capital that aligns with Islamic finance principles. Its transparent borrower ranges also help businesses quickly identify if the platform is a suitable fit for their needs.

Key Features and Insights

- Product Offerings: Specialises in Sharia-compliant SME business arrangements, offering amounts between AED 50,000 and AED 500,000 with monthly repayment plans.

- Application Process: The process is entirely online. SMEs submit an application with the required documents, which then undergoes a credit assessment by the Funding Souq team before a decision is made.

- Pricing: Specific rates and fees are provided only after a full application and risk assessment are completed.

- Pros: Fast decision-making process; strong regulatory credentials in the UAE and KSA.

- Cons: Funding is not same-day and requires underwriting; final pricing is not disclosed upfront.

Practical Insight: To get the fastest possible decision from Funding Souq, ensure all your business registration and financial documents are prepared and clearly organised before starting the application. A complete and accurate submission is key to their 72-hour approval target.

Find out more at Funding Souq.

4. Lendo

Lendo is a prominent digital invoice platform focused on the Saudi Arabian market. It offers a powerful solution for SMEs to manage their working capital by turning their outstanding invoices into cash. While not providing literal "instant funding," its process is significantly accelerated compared to traditional routes, with decisions typically made within 5-7 working days. The platform is designed specifically for invoice-based cash-flow needs, offering a fully digital workflow for businesses.

What makes Lendo stand out is its strong regulatory foundation and market focus. It is licensed by the Saudi Central Bank (SAMA) for debt crowdfunding activities, which provides a significant layer of credibility. This SAMA license ensures adherence to strict financial regulations. Lendo’s marketplace model connects SMEs directly with a pool of investors who fund the invoices, creating a competitive and transparent environment.

Key Features and Insights

- Product Offerings: Lendo specialises in digital invoice arrangements. This allows businesses to sell their unpaid invoices to investors at a discount, providing immediate liquidity. You can learn more about how invoice discounting works here.

- Application Process: The process is straightforward: SMEs register online, submit an application with their invoice, and Lendo’s team assesses it. Once approved, the invoice is listed on the platform for investors to fund.

- Pricing: The cost is determined by the invoice details and the business's risk profile. Specific rates are provided after the application and assessment are complete.

- Pros: Purpose-built solution for invoice-backed liquidity; high regulatory credibility due to SAMA licensing.

- Cons: Primarily focused on the KSA market; funding timeline depends on investor take-up and can take several days.

Practical Insight: To get the best outcome on Lendo, ensure your invoices are clear, accurate, and issued to reputable clients, as this increases investor confidence and the speed of funding.

Find out more at Lendo.

5. FlapKap

FlapKap is a prominent revenue-based platform tailored for e-commerce and digital-first SMEs across the MENA region. While not strictly offering "instant funding" in minutes, it delivers a rapid and non-dilutive solution for businesses to scale. Merchants connect their sales and advertising platforms, and based on this data, FlapKap generates an offer, typically within 2 to 5 working days. Once accepted, funds are usually available the next business day, making it a powerful tool for time-sensitive growth.

What makes FlapKap unique is its model, which is perfectly aligned with the cyclical needs of online businesses. Instead of demanding equity or fixed monthly repayments, FlapKap takes a percentage of future revenues until the advance and a pre-agreed flat fee are paid back. This flexible approach means repayments are higher during strong sales months and lower during quieter periods, protecting a business's cash flow. It is designed specifically for scaling inventory and marketing spend.

Key Features and Insights

- Product Offerings: FlapKap provides a revenue-based arrangement where businesses receive a cash advance in exchange for a percentage of their future sales, plus a single fixed fee.

- Application Process: The process is data-driven. E-commerce businesses connect their payment gateways, online stores, and digital advertising accounts. FlapKap's algorithm assesses performance to generate a customised offer.

- Pricing: The model is based on a transparent, fixed fee. There are no interest rates or late payment penalties. The fee is disclosed upfront with the offer.

- Pros: Fast advances aligned with marketing and inventory cycles; transparent fixed-fee structure with no equity dilution or late fees.

- Cons: Best suited for online sellers with consistent platform data; the process is fast but not instantaneous.

Practical Insight: To get the best offer from FlapKap, ensure your sales and marketing platform data is accurate and well-organised. A consistent history of revenue and a clear return on ad spend will likely result in a more favourable offer.

Find out more at FlapKap.

6. Tabby for Business

Tabby for Business is a leading Buy Now, Pay Later (BNPL) provider in the UAE and KSA that offers a unique approach to managing cash flow for merchants. Instead of traditional capital access, it accelerates merchant payouts, ensuring businesses receive their money on a predictable weekly cycle, regardless of when the end customer completes their payments. This structure transforms variable customer payments into a reliable revenue stream, making it a powerful tool for businesses aiming for more stable financial planning.

What makes Tabby for Business stand out is its direct impact on merchant cash collection and sales. By fronting the payment for customer purchases, Tabby absorbs the collection risk and simplifies the merchant's financial operations. This system not only improves cash flow but can also boost conversion rates and average order values by offering customers flexible payment options. For businesses in the UAE and KSA, this offers a practical way to achieve faster access to sales revenue.

Key Features and Insights

- Product Offerings: Tabby’s core service for businesses is its accelerated settlement process, where merchants are paid out on an agreed weekly cycle (fixed or flexible).

- Application Process: Merchants integrate Tabby as a payment option. Once live, settlements are managed via a dashboard where businesses can control payout options and thresholds in AED or SAR.

- Pricing: Fees apply to small settlements and on a per-payout basis. The exact fee structure is provided to merchants upon partnership.

- Pros: Creates predictable merchant settlements, improves cash collection, and can increase customer conversion and average order values.

- Cons: Payouts are cycle-based (weekly), not real-time per transaction.

Practical Insight: To maximise the benefits, merchants should align their operational expenses with Tabby’s weekly payout schedule to maintain consistent liquidity.

Find out more at Tabby for Business.

7. Tamara for Business

Tamara for Business is a leading GCC-born "Buy Now, Pay Later" (BNPL) platform that improves merchant cash flow. It provides businesses with regular, predictable payments. Merchants receive weekly settlements for all Tamara transactions, regardless of whether the end customer has completed their payments. This structure transforms fluctuating BNPL sales into a stable revenue stream, effectively providing an advance on customer receivables.

What makes Tamara for Business stand out is its strong regional presence and focus on simplifying merchant operations. By covering multiple markets like the UAE, KSA, Kuwait, and Bahrain, it allows businesses to offer flexible payment options to a wide customer base. The platform decouples merchant settlement from customer repayment schedules, removing the cash flow risk for the business and providing a form of instant funding on a weekly cycle. This is particularly valuable for e-commerce and retail businesses aiming for consistent capital to manage inventory and operations.

Key Features and Insights

- Product Offerings: The core offering is a BNPL payment solution for both online and in-store channels, with a key benefit being weekly settlements paid directly to the merchant.

- Application Process: Businesses can apply to become a Tamara partner through an online onboarding process. This typically involves an assessment of the business, and there may be a waitlist depending on demand.

- Pricing: Merchants are charged a fee per transaction. The specific rate depends on the business and is provided during the onboarding process.

- Pros: Creates predictable cash flow from BNPL sales; strong regional brand recognition and multi-channel support for merchants.

- Cons: Settlements are on a weekly schedule, not instantaneous per transaction; onboarding involves an approval process.

Practical Insight: To get the most out of Tamara, integrate it across all your sales channels, both online and in-store, to maximise customer adoption and ensure your weekly settlements reflect your total sales volume.

Find out more at Tamara for Business.

Instant Funding: Top 7 Comparison

To help you decide, here is a summary of the key aspects of each platform:

Comfi

- Implementation complexity: Low — plug-and-play, API & low-code plugins

- Resource requirements: Minimal internal IT; invoice data and onboarding docs

- Expected outcomes: Near-instant payment (typically <24h); improved cash flow and order sizes

- Ideal use cases: Wholesalers, suppliers, dealers, B2B marketplaces in MENA

- Key advantages: Instant approvals, high SME approval rate, offloads collections

Beehive

- Implementation complexity: Low–Medium — fully online onboarding

- Resource requirements: Basic documentation; online application

- Expected outcomes: Funding in days; faster than traditional banks

- Ideal use cases: UAE/GCC SMEs seeking working capital or invoice finance

- Key advantages: 100% online process, regional SME recognition, transparent messaging

Funding Souq

- Implementation complexity: Medium — regulated Sharia-compliant processes

- Resource requirements: Standard documentation; eligibility checks; cross-border compliance

- Expected outcomes: Quick approvals (guidance ~72h); term-based plans with scheduled repayments

- Ideal use cases: SMEs needing Sharia-compliant options in UAE and KSA

- Key advantages: Sharia-compliant products, DFSA & SAMA credentials, clear borrower ranges

Lendo

- Implementation complexity: Medium — invoice listing and investor workflow

- Resource requirements: Invoice documentation; platform registration; investor readiness

- Expected outcomes: Invoice funding via investors (typically ~5–7 working days)

- Ideal use cases: Saudi SMEs with invoice-backed cash-flow needs

- Key advantages: SAMA-licensed debt crowdfunding, invoice-focused liquidity

FlapKap

- Implementation complexity: Low–Medium — connect sales/ads platforms

- Resource requirements: Platform integrations and historical sales/ad data

- Expected outcomes: Offer in 2–5 days; funds next business day after acceptance

- Ideal use cases: E-commerce and digital-first merchants in MENA

- Key advantages: Revenue-based model aligned to cash cycles; fixed-fee structure

Tabby for Business

- Implementation complexity: Low — merchant integration and dashboard setup

- Resource requirements: Integration work; settlement configuration; merchant KYC

- Expected outcomes: Predictable weekly merchant settlements regardless of shopper payments

- Ideal use cases: Merchants in UAE/KSA using BNPL to boost conversion

- Key advantages: Predictable cash flow, increases conversion and AOV

Tamara for Business

- Implementation complexity: Medium — onboarding, multi-market setup

- Resource requirements: Integration, compliance checks; multi-market enablement

- Expected outcomes: Weekly settlements across GCC; predictable merchant cash flow

- Ideal use cases: Merchants across UAE, KSA, Kuwait, Bahrain offering BNPL

- Key advantages: Multi-country coverage, multi-channel acceptance, predictable payouts

Choosing the Right Partner to Accelerate Your Business

Navigating the landscape of SME capital in the UAE and wider MENA region reveals a powerful shift towards speed and accessibility. As we have explored, the term ‘instant funding’ encompasses a variety of solutions, from same-day invoice payouts with platforms like Comfi to peer-to-peer invoice trading and flexible business payment terms from providers such as Beehive, Lendo, and Tabby for Business. The traditional, lengthy process of securing capital is no longer the only path forward for ambitious small and medium-sized enterprises.

The key takeaway is that the right solution depends entirely on your unique business model. A wholesaler needing to unlock cash from large B2B invoices has different requirements than a retailer looking to offer flexible payment options at checkout. Your choice should align with your specific sales cycle, cash flow patterns, and strategic growth plans. Evaluating each option based on its speed, integration capabilities, approval criteria, and associated costs is crucial for making an informed decision.

Ultimately, the goal is to find a partner that not only provides capital but also acts as a catalyst for growth. Consider these critical factors before you commit:

- Speed of Payout: How quickly do you need the funds in your account? Does "instant" mean 24 hours, a few business days, or weekly settlements?

- Operational Integration: How easily does the platform integrate with your existing invoicing, accounting, or e-commerce systems? A seamless process saves time and reduces administrative burdens.

- Risk Management: Who assumes the risk of late or non-payment from your buyers? Platforms that take on this risk can provide significant peace of mind.

- Buyer Experience: How does the solution impact your customers? Offering flexible terms can be a powerful sales tool, so the process should be simple and clear for them.

By carefully considering these points, you can select an instant funding partner that empowers you to take control of your cash flow, serve your customers better, and confidently scale your operations. The right financial tools don't just solve a temporary cash gap; they build a more resilient and dynamic business for the future.

Ready to eliminate payment delays and accelerate your business growth? Discover how Comfi provides upfront payouts on your B2B invoices within 24 hours, allowing your business to unlock capital while offering your buyers the flexible payment terms they need. Visit Comfi to see how you can take control of your cash flow today.

Related Reading

- Your 2026 Guide to the 11 Best SME Business Loan Options in the UAE

- Finance Lender: How to Choose the Right Partner for SMEs

- 7 Faster Alternatives to a Traditional Business Loan

- Your Bank Statement: A Key to Unlocking Business Funding

Ready to improve your business cash flow? Get started with Comfi today.